Posted by Rob Swanke, Apr 23, 2021

Across the fixed income universe, the recent rise in interest rates hasn’t been equal.

Commonwealth’s Rob Swanke considers the implications for investors. The 10-year Treasury yield has been climbing steadily since hitting a low of 0.5 percent in August 2020. This week, as of April 20, it was close to 1.56 percent. But the rise in rates hasn’t been equal across the broad spectrum of fixed income instruments. If you’re an investor who hasn’t made any changes to your fixed income portfolio since last August, it’s likely your exposures have changed. As a result, your investments may not be delivering the benefits you’re looking for. To assess the situation, take a look under the hood at your fixed income portfolio. But first you need to understand what current interest rates are telling us—and how inflation is involved.

Rob Swanke considers the implications for investors. The 10-year Treasury yield has been climbing steadily since hitting a low of 0.5 percent in August 2020. This week, as of April 20, it was close to 1.56 percent. But the rise in rates hasn’t been equal across the broad spectrum of fixed income instruments. If you’re an investor who hasn’t made any changes to your fixed income portfolio since last August, it’s likely your exposures have changed. As a result, your investments may not be delivering the benefits you’re looking for. To assess the situation, take a look under the hood at your fixed income portfolio. But first you need to understand what current interest rates are telling us—and how inflation is involved.

Inflation Expectations

Given the reopening of state economies and federal stimulus being deployed into the market, many people have become concerned about the potential for rising inflation. (Recent posts on this topic can be found here and here.) Inflation had been muted until last month, when the March Consumer Price Index (CPI) reported year-over-year inflation of 2.6 percent. It was just a year ago, in March 2020, that inflation bottomed out, so this increase was expected.

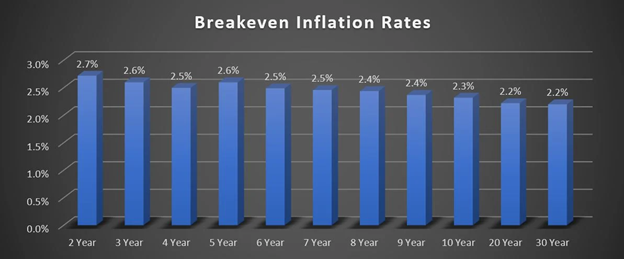

When assessing the potential for inflation to affect your investments, it’s important to understand what the market has already priced in. The graph below illustrates the inflation rates anticipated by the market. The expected difference in yield between Treasury yields and Treasury inflation-protected securities (TIPS) yields is charted for each bond maturity.

Across the fixed income universe, the recent rise in interest rates hasn’t been equal. Commonwealth’s Rob Swanke considers the implications for investors.

Source: Bloomberg, as of 4/20/2021

As you can see, the fixed income market has already priced in inflation of 2.7 percent for 2-year bonds—a rate very close to the March CPI number. In addition, the Fed has indicated it would let inflation run moderately above its stated 2 percent target for the time being, in order to make up for the recent stretch of low inflation. Inflation above 2 percent is exactly what the market is anticipating for the near term. In the longer term, the market expects inflation to fall closer to 2 percent.

What conclusion can be drawn? For fixed income investors, unexpected inflation rather than expected inflation should be the primary concern. With the market already pricing in inflation above the Fed’s target, a cushion for inflation pickup is in place.

Real Interest Rates

Fixed income yields are composed of two parts: inflation and the real rates of interest, which have been adjusted to remove inflation. Although the market is anticipating higher inflation, real interest rates have been negative recently for a good portion of the yield curve. In the chart below, the blue line represents 10-year Treasury yields and the orange line represents 10-year inflation expectations. The bottom panel shows the real interest rate falling into negative territory.

Across the fixed income universe, the recent rise in interest rates hasn’t been equal. Commonwealth’s Rob Swanke considers the implications for investors.

Source: Bloomberg

Prior to the pandemic, the Fed had been reducing its balance sheet to keep inflation from taking off. As a consequence, the real rates of interest were rising. When the pandemic hit, the combination of support from the federal government and the Fed eased conditions for borrowers. That meant the federal government could borrow money at rates lower than inflation, and firms could borrow money for very close to the level of inflation.

This environment can affect the profitability of companies. The effects of rising inflation can be passed on, but real rates of interest typically lead to higher costs that can’t be offset by raising prices. How does this affect investors? Currently, investors must accept a loss in purchasing power in order to buy Treasuries. The natural response of some investors is to move into riskier assets. I’ll look at the effects of that below.

Credit Spreads

The chart below shows the yield of the Bloomberg Barclays Corporate Index and the 10-year Treasury, with the spread between them illustrated in the bottom panel. While the maturities for these securities may not line up exactly, the story they tell is important. Over the past few months, as Treasury rates have been rising, corporate bond yields have barely budged. The result is a collapse in the spread between the two yields, which is now near its five-year low.

Across the fixed income universe, the recent rise in interest rates hasn’t been equal. Commonwealth’s Rob Swanke considers the implications for investors.

Source: Bloomberg

The story is the same when high-yield bonds are compared with investment-grade bonds. In March 2020, the yields of both investment-grade and high-yield bonds rose, but the yield of high-yield bonds went up more. Since then, the yields of both instruments have fallen. The spread between the two narrowed to close to its lowest point in the past 5 years and very close to its lowest point of the past 20 years (which occurred in 2007).

Across the fixed income universe, the recent rise in interest rates hasn’t been equal. Commonwealth’s Rob Swanke considers the implications for investors.

Source: Bloomberg

Over the past several months, investors who owned a mix of Treasuries and corporate bonds have seen the value of their Treasuries decline while the value of their corporate bonds has remained flat or increased. This has been especially true for investors holding high-yield securities, which are now more sensitive to an increase in credit risk. Portfolios incorporating fixed income have also become more sensitive to a rise in the general level of rates because yield spreads have less room to fall.

For example, with the duration of the investment-grade bond index currently at 8.5, if Treasury rates rise 1 percent and there is no decrease in the yield spread to offset the increase, the index would be expected to lose 8.5 percent. Earlier in the year, when rates rose, yield spreads fell, cushioning the loss for many portfolios. More recently, in March, the yields of corporate bonds rose along with those of Treasuries. As bond prices fall when yields rise, the result was a decline in value of both corporate bonds and Treasuries.

Implications for Investors

Going forward, an improving economy could mean that fixed income spreads will continue to narrow. The upside is minimal because spreads are already near their lows. In addition, the improving economy could cause real interest rates to increase more than the decrease in yield spreads. On the other hand, if we experience an economic pullback, yield spreads could widen much more than general interest rates fall. Any defaults by bond issuers could lead to losses for lower-quality bonds. Typically, lower-quality bonds have less sensitivity to rising Treasury rates. Since the great financial crisis, however, there have been several times that high-yield spreads have widened several percentage points, leading to significant losses for investors.

What does this mean for investors searching for yield? The best-case scenario for buying lower-quality bonds and reaching for their small amount of additional yield is a stable, flat, slow-growth economy. A more volatile environment may benefit investors holding lower-risk Treasuries and high-quality investment-grade bonds, combined with equities. Yes, there is a cost to holding bonds with negative rates of real interest. But these bonds could help provide a low-cost ballast for an equity portfolio through the potential for dividend payments as well as growth.

Bonds are subject to availability and market conditions; some have call features that may affect income. Bond prices and yields are inversely related: when the price goes up, the yield goes down, and vice versa. Market risk is a consideration if sold or redeemed prior to maturity.

Corporate bonds contain elements of both interest rate risk and credit risk. Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest, and, if held to maturity, they offer a fixed rate of return and fixed principal value. U.S. Treasury bills do not eliminate market risk.

© 2021 Commonwealth Financial Network®

© The Axial Company. All Rights reserved. 5 Burlington Woods, Suite 102 Burlington, Massachusetts

Disclosure: Certain sections of this commentary contain forward-looking statements based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Bloomberg Barclays Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Bloomberg Barclays government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities. The Bloomberg Barclays U.S. Corporate High Yield Index covers the USD-denominated, non-investment-grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.